All Categories

Featured

Table of Contents

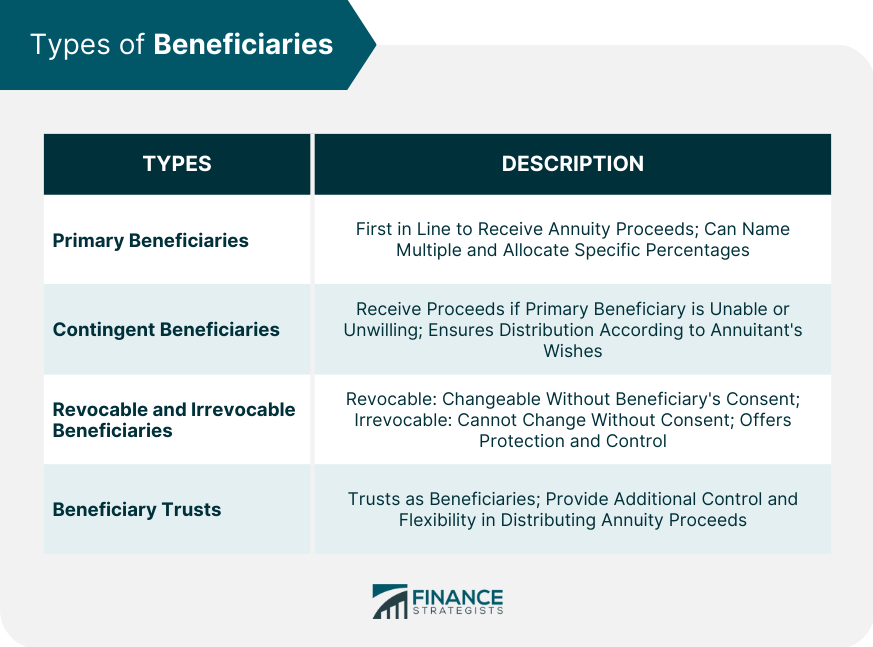

Generally, these conditions use: Owners can select one or numerous beneficiaries and specify the percent or dealt with amount each will receive. Beneficiaries can be individuals or organizations, such as charities, yet different regulations get each (see listed below). Proprietors can change beneficiaries at any type of point throughout the contract period. Owners can select contingent beneficiaries in instance a would-be heir passes away prior to the annuitant.

If a married couple owns an annuity jointly and one companion dies, the enduring partner would remain to get payments according to the terms of the agreement. Simply put, the annuity remains to pay out as long as one spouse continues to be to life. These contracts, in some cases called annuities, can additionally consist of a 3rd annuitant (typically a youngster of the pair), who can be assigned to get a minimum variety of payments if both companions in the original contract die early.

Are inherited Guaranteed Annuities taxable income

Right here's something to maintain in mind: If an annuity is sponsored by an employer, that organization needs to make the joint and survivor plan automated for pairs who are wed when retired life happens., which will impact your regular monthly payment in different ways: In this case, the month-to-month annuity repayment stays the very same complying with the death of one joint annuitant.

This sort of annuity may have been bought if: The survivor desired to handle the financial duties of the deceased. A pair took care of those obligations with each other, and the making it through partner intends to prevent downsizing. The enduring annuitant obtains just half (50%) of the month-to-month payment made to the joint annuitants while both were alive.

Immediate Annuities beneficiary tax rules

Lots of agreements permit a surviving partner provided as an annuitant's recipient to transform the annuity into their very own name and take over the preliminary arrangement., that is qualified to get the annuity just if the primary recipient is incapable or unwilling to accept it.

Squandering a lump sum will certainly trigger differing tax liabilities, depending upon the nature of the funds in the annuity (pretax or already taxed). However taxes won't be incurred if the partner remains to obtain the annuity or rolls the funds into an IRA. It may appear weird to assign a small as the recipient of an annuity, however there can be good factors for doing so.

In other instances, a fixed-period annuity might be made use of as a lorry to money a child or grandchild's college education. Minors can not inherit money directly. An adult must be marked to oversee the funds, similar to a trustee. Yet there's a difference between a count on and an annuity: Any cash appointed to a trust fund should be paid out within 5 years and does not have the tax advantages of an annuity.

A nonspouse can not typically take over an annuity agreement. One exception is "survivor annuities," which provide for that contingency from the inception of the contract.

Under the "five-year guideline," beneficiaries may delay claiming money for as much as 5 years or spread out payments out over that time, as long as every one of the cash is collected by the end of the fifth year. This permits them to expand the tax problem in time and may maintain them out of greater tax obligation braces in any kind of solitary year.

Once an annuitant passes away, a nonspousal beneficiary has one year to establish up a stretch circulation. (nonqualified stretch stipulation) This format establishes a stream of earnings for the remainder of the recipient's life. Since this is established over a longer period, the tax effects are normally the smallest of all the choices.

Tax consequences of inheriting a Joint And Survivor Annuities

This is occasionally the situation with immediate annuities which can begin paying promptly after a lump-sum financial investment without a term certain.: Estates, trust funds, or charities that are beneficiaries should take out the contract's amount within 5 years of the annuitant's fatality. Taxes are affected by whether the annuity was moneyed with pre-tax or after-tax bucks.

This just indicates that the money purchased the annuity the principal has actually already been exhausted, so it's nonqualified for tax obligations, and you do not have to pay the internal revenue service once more. Just the passion you make is taxable. On the other hand, the principal in a annuity hasn't been exhausted yet.

So when you take out money from a qualified annuity, you'll have to pay tax obligations on both the interest and the principal - Structured annuities. Proceeds from an acquired annuity are dealt with as by the Irs. Gross revenue is income from all resources that are not especially tax-exempt. But it's not the same as, which is what the IRS utilizes to establish just how much you'll pay.

If you inherit an annuity, you'll have to pay income tax on the distinction between the primary paid into the annuity and the worth of the annuity when the proprietor dies. For instance, if the owner bought an annuity for $100,000 and gained $20,000 in interest, you (the recipient) would certainly pay taxes on that $20,000.

Lump-sum payouts are strained all at once. This option has one of the most serious tax effects, since your revenue for a solitary year will certainly be much greater, and you may wind up being pressed right into a higher tax obligation brace for that year. Steady payments are exhausted as revenue in the year they are gotten.

, although smaller estates can be disposed of a lot more quickly (often in as little as 6 months), and probate can be even longer for more complicated cases. Having a legitimate will can speed up the procedure, yet it can still get bogged down if successors dispute it or the court has to rule on that need to carry out the estate.

Inherited Annuity Fees taxation rules

Since the individual is named in the contract itself, there's absolutely nothing to contest at a court hearing. It is essential that a specific person be named as beneficiary, rather than merely "the estate." If the estate is named, courts will certainly examine the will to arrange things out, leaving the will certainly open up to being disputed.

This might be worth considering if there are genuine worries about the individual named as recipient passing away before the annuitant. Without a contingent recipient, the annuity would likely then come to be based on probate once the annuitant dies. Talk to an economic expert concerning the possible benefits of naming a contingent recipient.

{kind=link}

Table of Contents

Latest Posts

Breaking Down Annuity Fixed Vs Variable A Closer Look at Fixed Vs Variable Annuity Pros Cons What Is the Best Retirement Option? Features of Deferred Annuity Vs Variable Annuity Why Choosing the Right

Analyzing Strategic Retirement Planning A Closer Look at How Retirement Planning Works Defining Variable Vs Fixed Annuities Pros and Cons of Various Financial Options Why Fixed Indexed Annuity Vs Mark

Exploring Fixed Income Annuity Vs Variable Growth Annuity A Closer Look at How Retirement Planning Works What Is the Best Retirement Option? Pros and Cons of Fixed Income Annuity Vs Variable Growth An

More

Latest Posts